What Is a Periodic Inventory System?

A periodic inventory system is a method of tracking inventory where the actual count and valuation of stock are performed at scheduled intervals rather than continuously. This approach, known as the periodic inventory method, involves counting inventory at set intervals and is cost-effective compared to perpetual systems.

It is particularly suitable for small businesses that do not require real-time inventory tracking. Think of it like taking a snapshot of your inventory at specific points in time rather than maintaining a real-time camera feed.

Definition and Explanation

A periodic inventory system is a method of inventory control that involves tracking inventory levels at specific intervals rather than continuously.

This system provides a snapshot of inventory levels at the end of a designated period, such as a month, quarter, or year. The periodic inventory system is often used by small businesses or those with limited inventory items, as it is a cost-effective and straightforward way to manage inventory. By conducting physical inventory counts at regular intervals, companies can determine their inventory balance and make necessary adjustments to their inventory records.

How Periodic Inventory Systems Work

A periodic inventory system tracks inventory levels through physical cycle counts, typically performed at the end of a designated period. The process involves counting the beginning inventory, tracking inventory purchases, and counting the ending inventory.

The balance in the purchases account is then transferred to the inventory account and adjusted to match the cost of the ending inventory.

This process provides a snapshot of inventory levels at the end of the period but does not provide ongoing updates between inventory counts. By relying on periodic physical counts, businesses can monitor inventory without continuous monitoring.

How Periodic Inventory Systems Works

At its core, a periodic inventory system operates through scheduled physical counts. During these predetermined intervals (monthly, quarterly, or annually), organizations conduct a complete count of all items in stock.

The beginning inventory plus purchases minus the ending inventory determines the cost of goods sold for that period. This calculation follows the formula:

Cost of Goods Sold = Beginning Inventory + Purchases – Ending Inventory

How It Works

- Physical Count: All inventory items are physically counted at the end of each designated period. This involves counting the actual quantities of each item on hand.

- Inventory Valuation: Once the physical quantities are known, the value of the inventory is calculated using a cost flow assumption like FIFO (first-in, first-out), LIFO (last-in, first-out), or weighted average cost. The chosen method is applied to assign costs to the counted inventory.

- Cost of Goods Sold Calculation: The cost of goods sold for the period is then calculated using this formula: Beginning Inventory + Purchases – Ending Inventory = Cost of Goods Sold. Beginning inventory is the ending inventory from the previous period. Purchases include all inventory acquired during the current period. Ending inventory is the total inventory value on hand based on the physical count at the end of the period.

- Financial Reporting: The calculated cost of goods sold is reported on the income statement for the period. The ending inventory value is reported as a current asset on the balance sheet.

Application in Maintenance Organizations

Periodic inventory systems serve specific functions in maintenance settings. For instance, a facilities maintenance department might use this system to track spare parts, tools, and consumable materials.

The periodic nature allows maintenance teams to focus on their primary duties while maintaining inventory control through regular audits. Inventory counts and reporting align with the timing of the accounting period, influencing the accuracy of financial statements.

Consider a building maintenance team that manages replacement parts for HVAC systems. They might conduct monthly inventories of critical components like filters and refrigerants while doing quarterly counts of less frequently used items like fan motors or control boards. This tiered approach helps balance operational efficiency with inventory accuracy.

A periodic inventory system can be used in maintenance organizations to track and value spare parts and maintenance, repair, and operating (MRO) supplies. Here’s how it applies:

- Spare Parts Inventory: Maintenance organizations keep an inventory of spare parts to service equipment and machinery. A periodic system involves regularly counting these parts to determine quantities on hand.

- MRO Supplies: Consumable supplies used in maintenance activities, like lubricants, cleaning agents, and personal protective equipment, are also tracked using periodic inventory counts.

- Budgeting and Cost Control: Maintenance managers can assess inventory levels against target stocking quantities by conducting periodic counts. This helps control costs by identifying excess inventory or stock-outs that require replenishment.

- Work Order Costing: When maintenance work orders are completed, the associated spare parts and supplies consumed are relieved from inventory. Periodic counts ensure accurate tracking of these costs.

- Financial Reporting: The periodic system allows maintenance organizations to report the value of their spare parts and MRO inventory on financial statements, which is essential for budgeting, cost analysis, and overall financial management.

Comparison with Other Inventory Systems

Perpetual Inventory System

Unlike periodic systems, the perpetual inventory method provides real-time tracking of stock levels using technology such as POS systems and RFID scanners.

Every transaction, including sales, returns, and restocks, is recorded immediately, offering constant visibility into inventory status. Modern computerized systems often use barcode scanners or RFID technology to maintain this continuous record.

The key difference lies in timing and accuracy. While a perpetual system might show you have ten air filters in stock at any moment, a periodic system would only confirm this during scheduled counts. However, perpetual systems require more sophisticated technology and ongoing attention to transaction recording.

Just-In-Time (JIT) Inventory

JIT systems represent a fundamentally different approach, focusing on minimizing inventory by ordering items only when needed. This method reduces carrying costs but requires reliable suppliers and accurate demand forecasting. In maintenance operations, JIT can be challenging due to the unpredictable nature of equipment failures and repair needs.

ABC Inventory Method

This system categorizes items based on their value and importance. While not mutually exclusive with periodic inventory, ABC analysis can complement it by determining count frequencies. Critical A-items might receive monthly counts, while less crucial C-items could be counted annually.

Advantages of Periodic Inventory in Maintenance

- Lower administrative burden compared to perpetual systems

- Simpler implementation requiring less technological infrastructure

- Performing physical inventories is crucial to verify the accuracy of ledger data.

- Regular physical counts help identify damaged or obsolete items

- Opportunity to clean and organize storage areas during counts

- Better suited for organizations with predictable usage patterns

Disadvantages of Periodic Inventory Systems

While periodic inventory systems have some advantages, they also have some disadvantages. One of the main disadvantages is that they do not provide real-time updates on inventory levels, which can lead to stockouts or overstocking.

Additionally, periodic inventory systems can be prone to errors and inaccuracies, mainly if the physical counts are not performed accurately.

Furthermore, periodic inventory systems may not be suitable for larger businesses or those with complex inventory requirements, as they can be time-consuming and labor-intensive. The lack of continuous inventory tracking can make it challenging to maintain optimal inventory levels and respond quickly to changes in demand.

Challenges and Considerations

The periodic approach does have limitations. Between counts, stock levels are essentially estimates, which can lead to stockouts or overordering. Maintenance organizations must carefully balance the frequency of counts with operational demands.

Critical spare parts might warrant more frequent counting or a hybrid approach using perpetual tracking for select items.

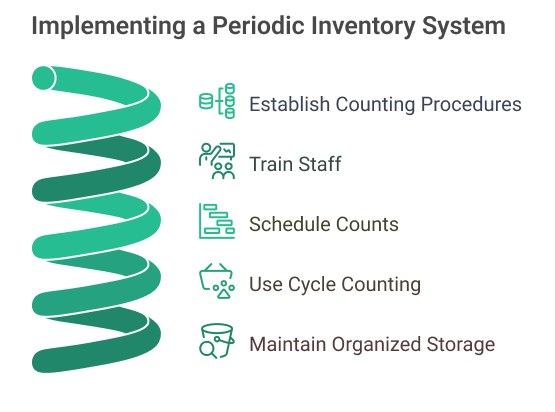

Implementing a Periodic System

Success with periodic inventory requires thoughtful planning. Inventory transactions are documented by debiting the purchase account when recording the purchase of inventory. Organizations should:

- Establish clear counting procedures and documentation methods

- Train staff in proper counting techniques and record-keeping

- Schedule counts during lower-activity periods when possible

- Use cycle counting for different categories of items

- Maintain organized storage to facilitate accurate counts

Modern Adaptations

Today’s maintenance organizations often blend periodic inventory with digital tools. Mobile devices can streamline counting processes, while inventory management software can help analyze usage patterns and suggest optimal counting frequencies. This hybrid approach maintains the simplicity of periodic inventory while leveraging technology for better accuracy and efficiency.

The choice between inventory systems ultimately depends on an organization’s needs, resources, and operational patterns.

Periodic inventory continues to be a practical solution for many maintenance operations, particularly when combined with modern tools and thoughtful implementation strategies. Would you like me to elaborate on any particular aspect of these inventory systems?

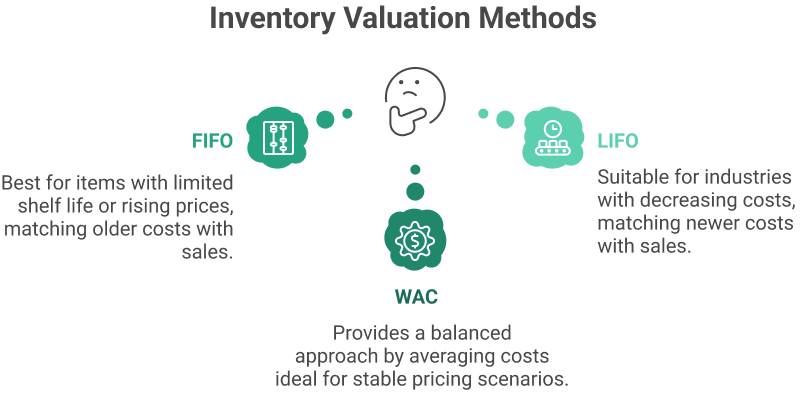

Inventory Valuation Methods

Inventory valuation methods determine the cost of goods sold and ending inventory in a periodic inventory system. There are several inventory valuation methods, including:

- First-In, First-Out (FIFO): This method assumes that the oldest inventory items are sold first. It is often used when inventory items have a limited shelf life or when prices are rising, as it matches older, lower-cost items with current sales.

- Last-In, First-Out (LIFO): This method assumes that the most recent inventory items are sold first. It is commonly used in industries where inventory costs decrease, matching newer, higher-cost items with current sales.

- Weighted Average Cost (WAC): This method uses an average cost to assign the ending inventory value. It is calculated by dividing the total cost of goods available for sale by the total number of units available for sale, providing a balanced approach to inventory data and valuation.

Each method has its own advantages and is chosen based on the business’s specific needs and circumstances.

By selecting the appropriate inventory valuation method, businesses can ensure accurate financial reporting and effective inventory management within a periodic inventory system.

Get a Free WorkTrek Demo

Let's show you how WorkTrek can help you optimize your maintenance operation.

Try for free